Many UAE businesses lose thousands of dirhams every year simply because they don’t claim VAT correctly. Imagine walking past a stack of cash on the sidewalk every single day and just… leaving it there. That is exactly what happens when a business fails to optimize its input tax recovery.

In the high-speed economy of Dubai and the wider UAE in 2026, VAT indirect tax is no longer a “new” concept, yet it remains one of the most misunderstood levers of cash flow. Input VAT recovery isn’t just a compliance checkbox; it is a direct injection of liquidity back into your business. If you’ve paid it to a supplier, you likely have a right to get it back provided you play by the Federal Tax Authority’s (FTA) rules.

This guide will break down the “what, why, and how” of recovering your tax, ensuring you never leave money on the table again.

What Is Input Tax Recovery in the UAE?

To understand recovery, we first have to look at the nature of VAT indirect tax.

Value Added Tax is an indirect tax because the ultimate economic burden falls on the final consumer, not the business. However, businesses act as the government’s collection agents.

- Input VAT: The 5% tax you pay when you buy goods or services for your business (e.g., office rent, stock, or software).

- Output VAT: The 5% tax you collect when you sell your goods or services to your customers.

- Recovery: The process of “offsetting” the tax you paid (Input) against the tax you collected (Output).

The goal of the UAE’s VAT system is that a business should only pay the difference to the FTA. If your Input VAT is higher than your Output VAT in a specific period, the government actually owes you a refund.

How VAT Indirect Tax Works? The Simple Flow

Think of VAT as a relay race where the “tax baton” is passed from the manufacturer to the wholesaler, then the retailer, and finally the consumer.

A Practical Example

Suppose you run a consulting firm in Dubai:

- The Purchase: You buy new laptops for your team for AED 10,000. You pay AED 500 in VAT to the electronics store. This is your Input VAT.

- The Sale: You provide a strategy report to a client for AED 20,000. You charge them AED 1,000 in VAT. This is your Output VAT.

- The Offset: When it’s time to file your return, you don’t give the FTA the full AED 1,000. You subtract the AED 500 you already paid.

The formula for your tax liability is:

$$VAT_{payable} = VAT_{output} – VAT_{input}$$

$$VAT_{payable} = 1,000 – 500 = 500 \text{ AED}$$

By recovering that AED 500, you’ve protected your profit margin.

Conditions to Claim Input VAT (The Golden Rules)

The FTA doesn’t just take your word for it. To legally claim back VAT indirect tax, you must satisfy four strict criteria. If even one is missing, your claim is a “red flag” for an audit.

The Recovery Checklist:

- Recipient of Goods/Services: You (the business) must be the one who actually received the supply.

- Taxable Supplies: The expense must be used to make “taxable supplies.” If your business is exempt (like certain residential real estate), you generally cannot recover VAT.

- Intention to Pay: You must intend to pay the supplier within six months.

- The Holy Grail (The Valid Tax Invoice): You must hold a full or simplified tax invoice that meets all FTA requirements (TRN, date, VAT amount, etc.). No invoice, no recovery. No exceptions.

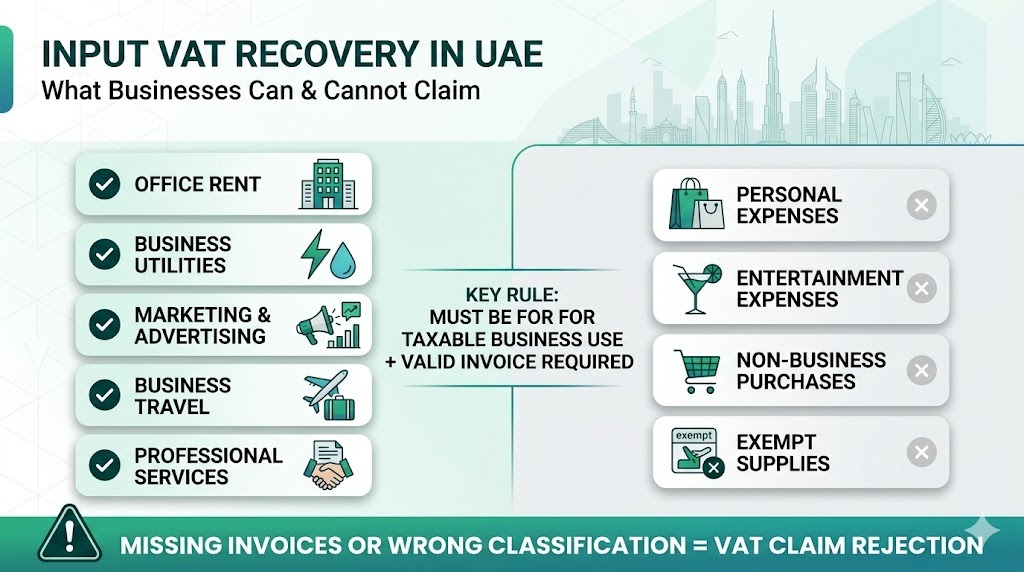

What You CAN and CANNOT Claim?

This is where most businesses stumble. Just because an expense is “for the company” doesn’t mean the VAT is recoverable.

| Expense Type | VAT Recoverable? | Notes |

| Office Rent & Utilities | Yes | Must be a commercial space. |

| Marketing & Advertising | Yes | Agency fees, social media ads, etc. |

| Inventory & Raw Materials | Yes | For goods intended for resale. |

| Fuel (Business Vehicles) | Yes | Only for vehicles used exclusively for business. |

| Entertainment Expenses | No | Staff parties, client dinners, and “hospitality.” |

| Personal Expenses | No | Your weekend groceries or personal car. |

| Exempt Activities | No | Expenses related to non-taxable income. |

Note: Entertainment is the biggest trap. If you take a client to a fancy dinner in the Marina, that 5% VAT is a sunk cost. The FTA views this as non-essential for the core “taxable supply” process.

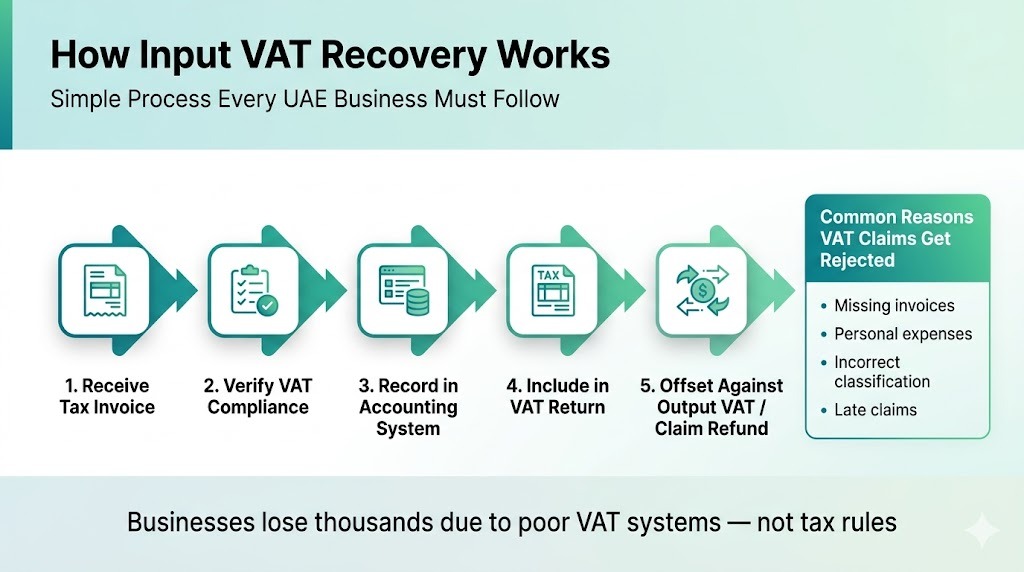

Step-by-Step VAT Recovery Process

To maximize your recovery, you need a workflow that catches every single dirham.

- Receive Supplier Invoice: Check it immediately. Does it have your company name? Is the TRN correct?

- Verify Compliance: Ensure the VAT is calculated correctly at 5%.

- Record in Accounting System: Log the expense under the correct “Input VAT” account.

- Classify Correctly: Separate recoverable VAT from non-recoverable VAT (like entertainment) right at the entry stage.

- Include in VAT Return: Your return will sum up all eligible Input VAT for the period.

- Offset & Reconcile: Ensure your books match your FTA portal submission.

Real-Life Scenarios: Why Claims Get Rejected?

Scenario 1: The Pro-forma Blunder

A logistics company claimed AED 50,000 in Input VAT based on a “Pro-forma Invoice.”

- The Problem: Pro-forma invoices are quotes, not tax documents.

- The Mistake: The FTA rejected the claim during a desk audit because a “Tax Invoice” was never issued.

- Correct Approach: Always insist on a final Tax Invoice before filing your return.

Scenario 2: The Missed Deadline

A retail chain found an invoice from three years ago that they forgot to claim.

- The Problem: They tried to slip it into their 2026 return.

- The Mistake: Claims must generally be made in the period the invoice was received or the immediate next period.

- Correct Approach: Use the “Voluntary Disclosure” process if the amount is significant, but realize there are strict time limits.

Partial VAT Recovery Explained

What happens if your business makes both taxable and exempt sales? This is known as “Mixed Supplies.”

If you run a building that has commercial shops (taxable) on the ground floor and residential apartments (exempt) above, you cannot claim 100% of the VAT on the building’s maintenance. You must “apportion” the VAT.

The basic concept is:

$$\text{Recoverable VAT} = \text{Total Input VAT} \times \left( \frac{\text{Taxable Turnover}}{\text{Total Turnover}} \right)$$

It’s a bit more nuanced than that, but the takeaway is simple: if you have mixed income, you need an expert to calculate your “Recovery Ratio.”

Time Limits & Deadlines (2025–2026 Update)

In 2026, the FTA is more digital than ever. The primary rule remains: you should claim Input VAT in the first tax period in which the invoice is received and the intent to pay is formed.

- The 5-Year Rule: There is a statute of limitations. Generally, you cannot reach back further than 5 years to correct or claim VAT.

- The “Two-Period” Window: If you miss an invoice in Period A, you can usually claim it in Period B. If you miss Period B, you often have to file a Voluntary Disclosure (VD), which can attract administrative fees.

Missed VAT = Permanent Loss. Every month you wait is a month closer to that money disappearing forever.

What To Do If You Miss or Lose VAT Claims

If you’ve discovered a pile of unclaimed invoices from last year, don’t panic but don’t wait.

- Audit Your Past Returns: Identify exactly how much was missed.

- Check the Value: If the error is under AED 10,000, you can usually correct it in your next return. If it’s over AED 10,000, you must file a Voluntary Disclosure.

- Prepare Documentation: Ensure you have the physical invoices ready for inspection.

- Seek Professional Help: Filing a Disclosure triggers FTA scrutiny. You want your paperwork to be bulletproof.

FTA Audits & Red Flags

The FTA’s AI systems are designed to spot “unusual” patterns. Here are the red flags that trigger an audit:

- Consistent Refunds: If your Input VAT is always higher than your Output VAT, the FTA will want to know why.

- Frequent Adjustments: Constantly changing your filed returns suggests poor vat tax accounting systems.

- High “Entertainment” Claims: If you try to claim VAT on staff lunches or luxury gifts, the system will flag it.

A System to Maximize Your VAT Recovery

Stop relying on luck. Implement this “Recovery System”:

- Digital Invoice Tracking: Use software that scans invoices (like OCR technology) to ensure data entry is 100% accurate.

- Monthly Reconciliation: Never wait until the end of the quarter. Match your invoices to your bank statement every 30 days.

- Staff Training: Ensure your procurement team knows not to accept invoices that don’t have your company’s TRN.

- The Six-Month Rule Check: Review your accounts payable. If you haven’t paid a supplier in 6 months, you might have to “reverse” the VAT you claimed.

VAT Myths & Misconceptions

- Myth: “I can claim VAT on my personal car because I drive it to the office.”

- Fact: Only vehicles used exclusively for business (like delivery vans) qualify.

- Myth: “As long as I have a receipt, I can claim it.”

- Fact: A “receipt” from a cash register is often not a “Tax Invoice.” It must meet the FTA’s specific labeling requirements.

- Myth: “VAT recovery is automatic.”

- Fact: You must actively calculate and report it. The FTA will never “remind” you to take your money back.

When Should You Hire a VAT Expert?

If your business is growing, your tax complexity is growing with it. You should seek expert advice if:

- You are confused by “Reverse Charge Mechanisms” on imports.

- You are dealing with “Mixed Supplies” and partial recovery.

- You’ve received a notification from the FTA and don’t know how to respond.

- You suspect you’ve been leaving thousands of dirhams in unclaimed VAT on your books.

How Dubai Business and Tax Advisors Helps

Recovering your VAT indirect tax shouldn’t be a headache.it should be a payday. At Dubai Business and Tax Advisors, we act as your financial shield and your recovery engine.

- Optimization: We deep-dive into your expenses to find every eligible claim you’ve missed.

- Compliance: We ensure your invoices are 100% FTA-compliant to prevent rejections.

- Voluntary Disclosures: If you’ve made mistakes in the past, we fix them with minimal penalty risk.

- Audit Representation: We handle the FTA so you can handle your business.

Frequently Asked Questions

What is input tax recovery and how does it work in the UAE?

Input tax recovery allows VAT-registered businesses to reclaim VAT paid on business purchases and expenses from the Federal Tax Authority (FTA). When you buy goods or services for your business, you pay 5% VAT to suppliers, which becomes recoverable input tax. You claim this back by offsetting it against output VAT (VAT you collect from customers) on your quarterly VAT return. This prevents double taxation and ensures businesses only pay VAT on the value they add.

What expenses can I claim input tax recovery on?

You can recover VAT on any business-related purchases including office rent, equipment, supplies, professional services, utilities, software subscriptions, and business travel. The expense must be wholly for business purposes and supported by valid tax invoices showing the supplier’s TRN and correct VAT amount. Personal expenses, entertainment costs exceeding certain limits, and purchases from non-registered suppliers are generally not recoverable.

Are there any expenses where input tax recovery is blocked or restricted?

Yes. Input tax cannot be recovered on certain blocked expenses including motor vehicles not used solely for business, some entertainment and hospitality costs, and residential property purchases. Additionally, if you make exempt supplies (like residential property rentals or financial services), you cannot recover input tax related to those activities. The FTA provides specific guidance on blocked input tax categories that businesses must follow.

What documentation do I need to support my input tax recovery claims?

You must have valid tax invoices from VAT-registered suppliers showing their TRN, your business details, invoice date, description of goods/services, VAT amount, and total amount. Invoices must be genuine, accurate, and retained for at least five years. Claiming input tax without proper documentation will be rejected during FTA audits and can result in penalties, repayment demands, and interest charges.

What happens if I claim input tax recovery incorrectly or fraudulently?

Incorrect claims discovered during FTA audits result in the recovery being reversed, plus penalties of 50% of the incorrectly recovered amount for unintentional errors. Deliberate fraudulent claims can trigger penalties up to 300% of the tax involved, criminal prosecution, and potential imprisonment. The FTA uses sophisticated data analytics to detect irregular recovery patterns, so all claims must be legitimate, accurate, and properly documented.

Conclusion

VAT recovery is one of the few areas where the tax law is designed to give you money back. In the competitive landscape of the UAE, every percentage point of margin matters. Leaving your Input VAT unclaimed is essentially giving your competitors a head start.

Don’t let “compliance fear” stop you from accessing your own cash flow. Set up the right systems, keep your invoices tight, and if the rules feel too complex, let Dubai Business and Tax Advisors handle the heavy lifting.

Ready to recover the VAT you’re entitled to? Contact Dubai Business and Tax Advisors today for a comprehensive review of your last three months of expenses. We’ll identify missed recoverable VAT opportunities and implement systems to maximize your input tax recovery going forward.

Stop leaving money on the table and get expert support from Dubai Business and Tax Advisors now.